BCOM 1st Year Branch Account Long Question Answer Study Material Notes

BCOM 1st Year Branch Account Long Question Answer Study Material Notes

Q.4. What do you mean by independent branch? What journal entries are made in the books of head office to incorporate branch trial balance? (2015)

Ans. Independent Branch

The branches that keep their accounts independently and carry out their business independently under the policies laid down by the head office are known as independent branches. An independent branch never means that it does not depend on the head office at all. In fact, a branch can never be independent of H.O. The independence of a branch is referred to merely ‘Independence in accounting function’. Hence, a branch is called independent only when it is allowed to maintain full accounting system, so as to be in a position to extract its own trial balance, prepare its own trading and profit & loss account and balance sheet in usual manner.

Salient Features of Independent Branches

The following are the salient features of independent branches:

1. Independent branches keep a complete set of books of accounts.

2. It does not confine its trading to the go

3. It may make purchases on its own account and can affect cash and credit sales.

4. It operates as an independent business for all practical purposes except that it has to follow certain broad policies as laid down by head office.

5. It keeps its own banking account and remittances to and from head office to the need.

6. It keeps its own final accounts at the end of accounting year.

7. The connection between the head office and the branch bokkeeping system is maintained by means of: (a) a branch account in the head office books and (b) a head office account in the branch books.

Incorporation of Branch Trial Balance in the H.O. Books

After recording all the transactions properly, independent branch prepares its trial balance at the end of the accounting year and send a copy of it to the head office so that the head office may include it in its books to present a complete picture of the whole business. For this purpose, H.O. passes certain entries to unite the accounting information of the branch trial balance with its own books. This process is called ‘Incorporation of branch trial balance’.

Following are the three alternative methods of doing so:

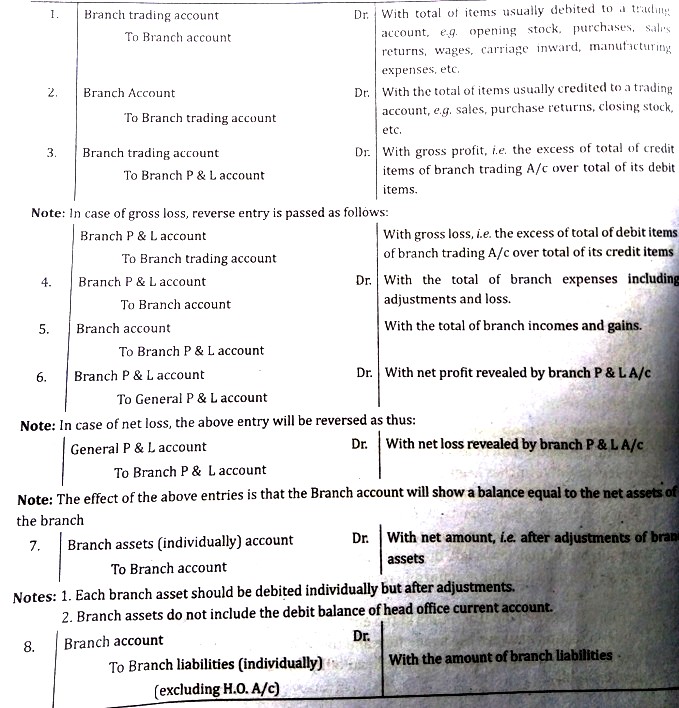

- First Method: The most popular method of incorporation is such that Trading and Profit & Loss Account of the branch is prepared in the head office ledger in a regular way. The following entries are passed for this purpose:

Notes: 1. Each branch liability should be shown individually. 2. Branch liabilities do not include the credit balance of head offic 3. After passing entries (7) and (8), the branch account will balance off,

At the commencement of the next accounting these assets and liabilities to the books of branch.

2. Second Method: Instead of passing eight entries as under first method above, only entries may be passed to incorporate the entire trial balance.

(a) All debit items in branch trial balance (individually)

Dr. To Branch account:

(For incorporation of all debit items in branch trial balance)

(b) Branch account

Dr. To All credit items in branch trial balance (except H.O.AI)

(For incorporation of all credit items in branch trial balance)

Note: Head orice current account in the branch trial balance is excluded from incorporation in the above entries.

3. Third Method: Under this method, the branch Trading and Profit & Loss Account is prepared only as a memorandum account and the following entries are passed for incorporating branch net profit or loss and assets and liabilities of the branch:

- Branch account Dr.

To General P&L account

(For incorporation of branch net profit)

Note: In case of net loss, the above entry is reversed as follows:

General P&L account

(For incorporation of branch net loss) Dr.

(b) Branch assets (individually) Account

To Branch account

(For incorporation of branch assets)

(c) Branch account

To Branch liabilities (individually)

(For incorporation of branch liabilities)

Note: All the assets and liabilities of the branch are incorporated individually and after all adjustments but the balance of head office account is excluded.

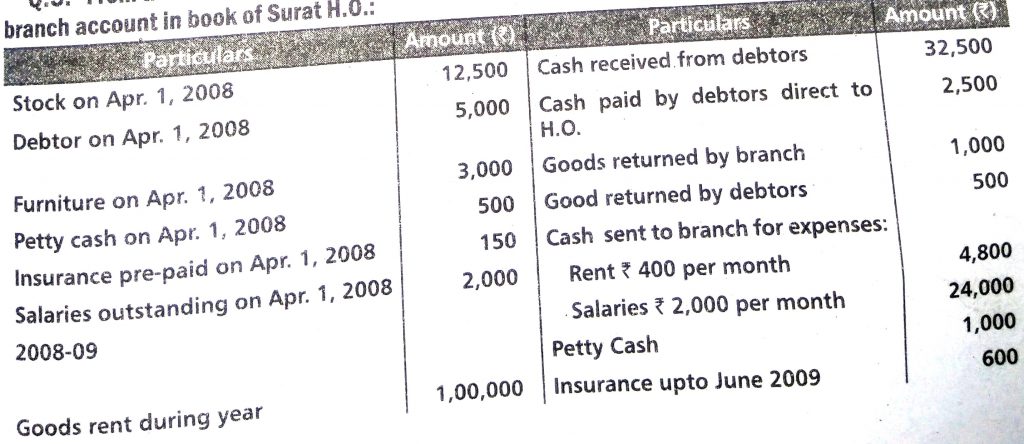

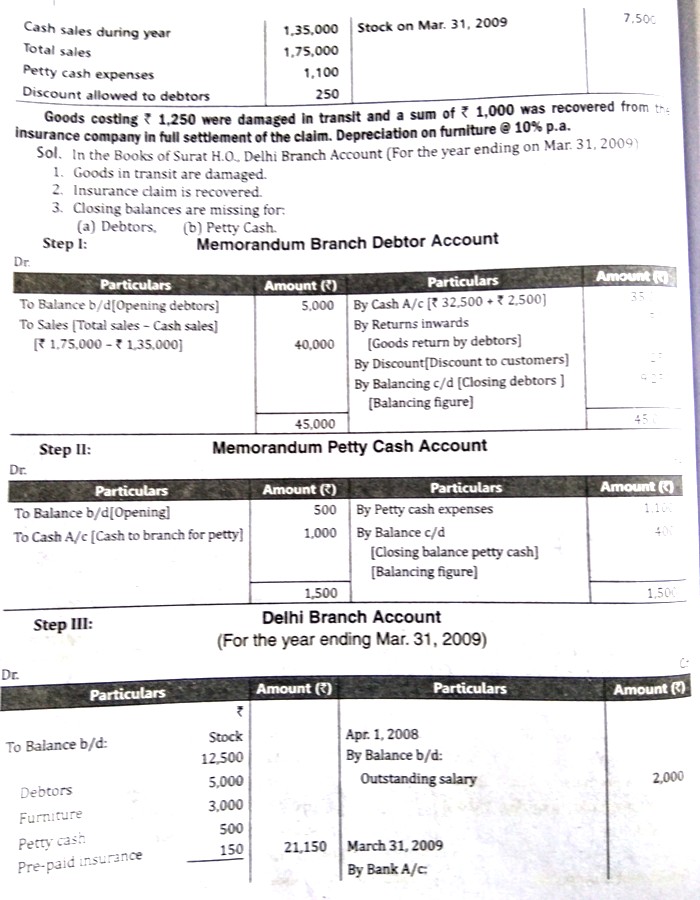

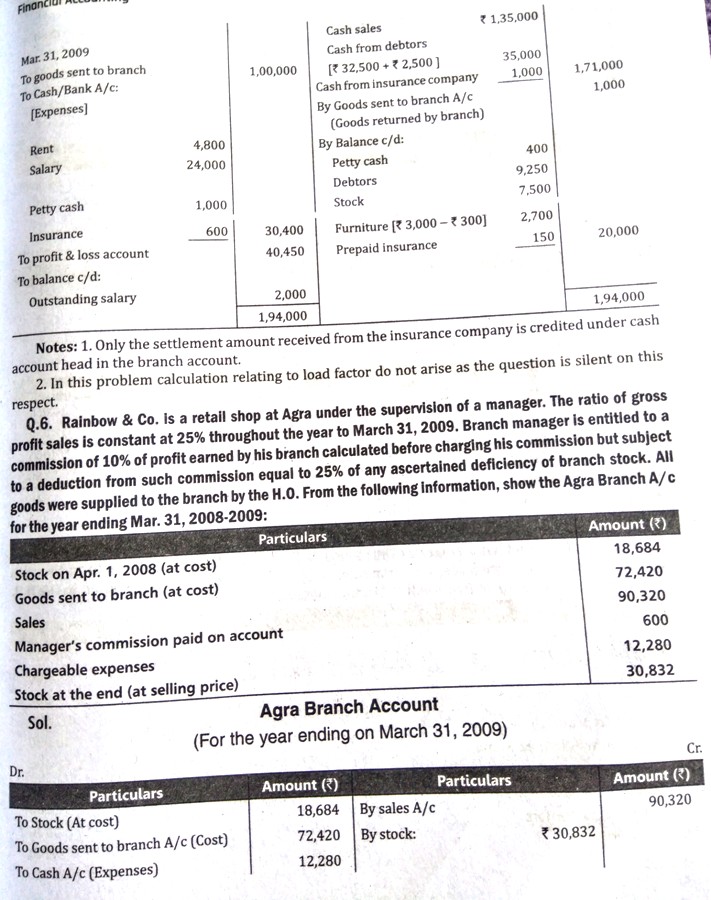

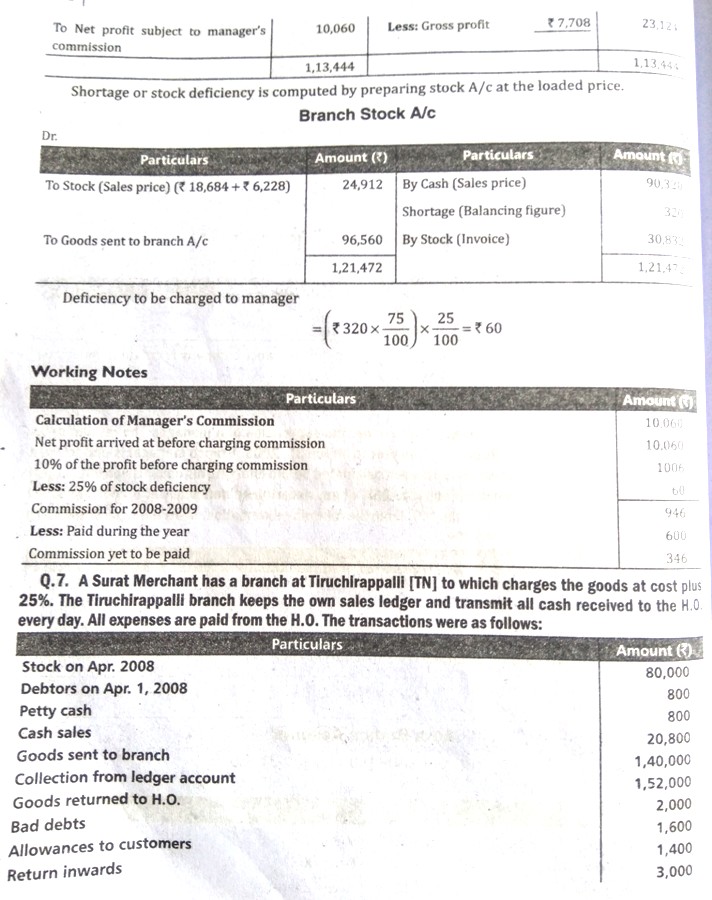

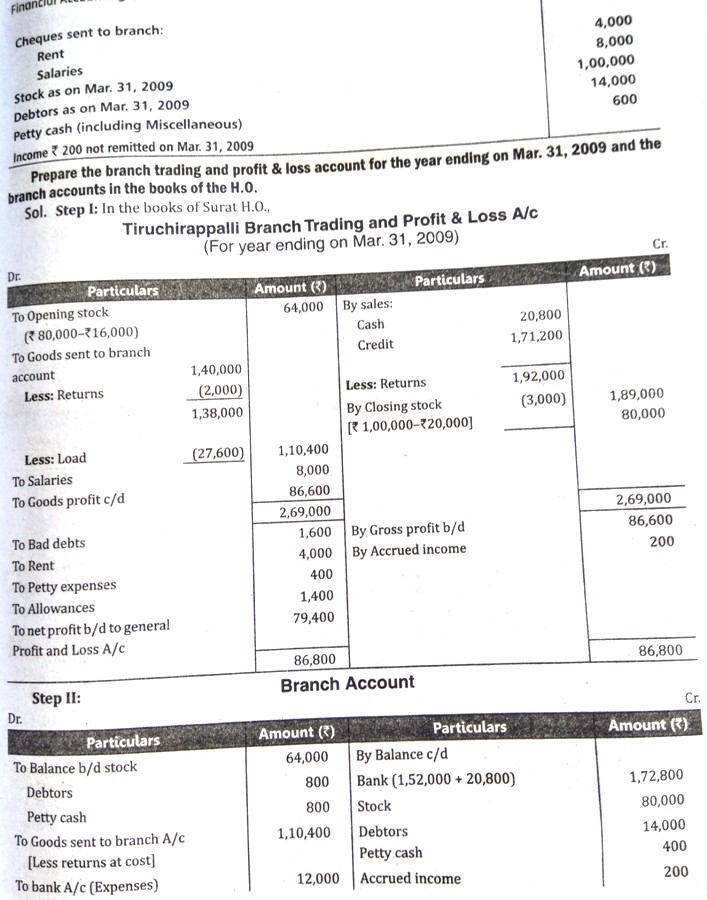

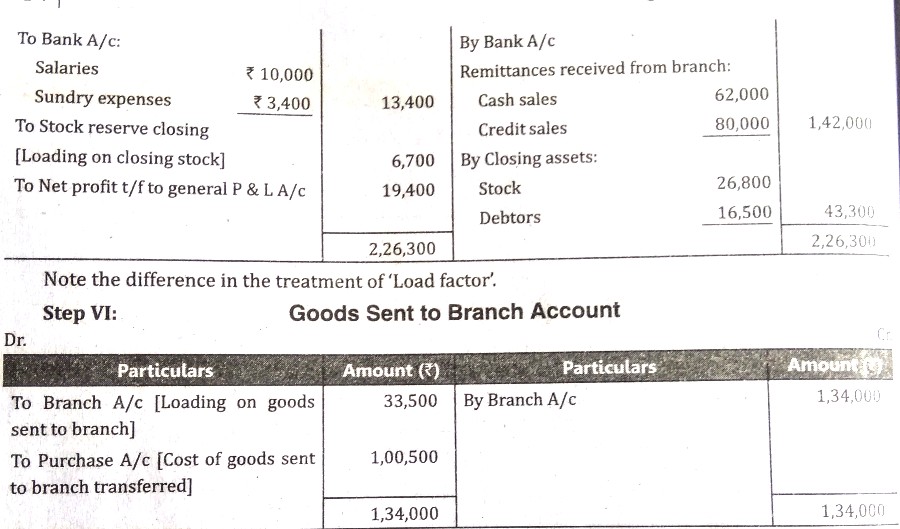

Q.5. From the following details relating to Delhi branch for the year ending Mar. 31, 2009, prepare the branch account in book of Surat H.O.:

B.Com Ist Year Foreign Trade And Economic Growth Question Answer Notes

[PDF] B.Com 1st Year All Subject Notes Study Material PDF Download In English

B.Com 2nd Year Books Notes & PDF Download For Free English To Hindi

B.Com 1st Year Notes Books & PDF Free Download Hindi To English

B.Com 1st 2nd 3rd Year Notes Books English To Hindi Download Free PDF

B.Com Ist Year Unemployment Short Study Notes Question Answer

Follow Me

Leave a Reply